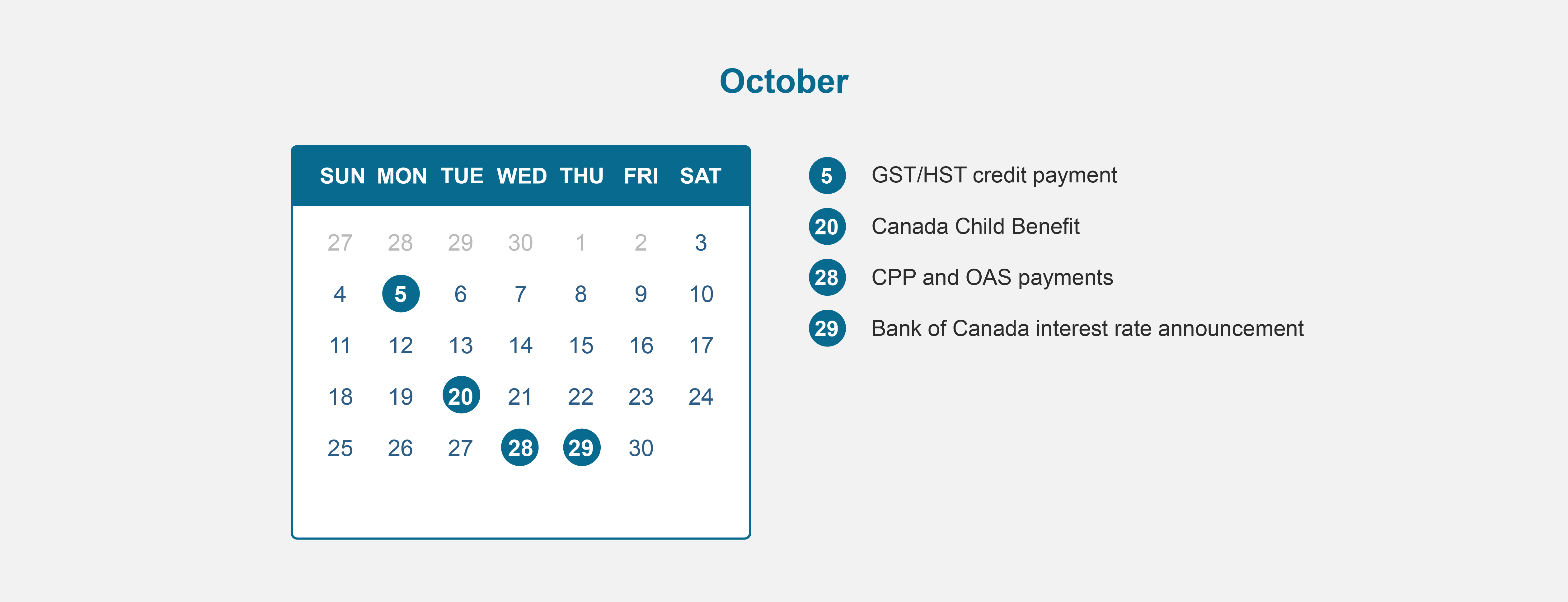

How to Make the Best of Inheritance Planning

How to Make the Best of Inheritance Planning

Inheriting an unexpected, or even an anticipated, lump sum can fill you with mixed emotions – if your emotional attachment to the individual who has passed away was strong then you are likely to be grieving and the thought of how to handle your new-found wealth can be overwhelming and confusing but also exciting. One of the best pieces of advice in this situation is to give yourself some time before making any binding financial decisions. The temptation to quickly put the money to so-called ‘good use’ or to rush out and spend it can be strong but you must allow the news to sink in and also take some time to consider your options before you embark on the process of dealing with the inheritance. In the short term, put the money away in a high interest savings account and take time to research and think carefully about your financial goals and objectives and how this inheritance can help you to secure and maximize your financial future in the best way.

Although there is no one-size-fits-all approach to dealing with larger sums of money, here are some useful ideas of where to start.

Reduce your debt burden

If you have significant or high-interest debts, one of the safest options of all is paying this debt down. Not only will you achieve a guaranteed after-tax rate of return of your current interest rate, it can also add to your feeling of financial security and potentially offer you a more consistent financial picture. Debt often carries with it a significant interest rate – particularly on credit cards and overdrafts for example – so in many cases, eliminating this burden should be considered as one of your main priorities.

However, you may like to take careful note of the option below regarding investing the money instead as much depends on the prevailing interest rates and, of course, your appetite for risk, as you may well find an investment option with a potentially higher return more attractive.

Make investments

A particularly effective way of investing an inheritance is to add it to your retirement savings – especially if your nest egg is not looking quite as healthy as it should due to missed savings years for example. Those with lower or less reliable incomes should look upon this option as a great choice in particular.

Be charitable

After considering your own future financial needs, giving some of your wealth away to either charities or to family and friends is a good option to share out some of your inheritance to those who could benefit from it. What’s more, donating to charity can also offer you some tax breaks which may reduce your overall tax burden.

Many individuals see this philanthropic route as offering them the opportunity to do something meaningful and rewarding with their wealth and contributing towards their own sense of moral duty and emotional wellbeing.

Make a spending plan

Of course, you are likely to be keen to spend some of your wealth on yourself and your family, particularly if your financial situation means that you have previously had to be more careful and prudent with money than you would have liked. A great way to do this is to create a spending plan so that you can enjoy the benefits of spending, without it significantly eating into money set aside for your financial planning goals. You could, perhaps, aim to set aside 10% of the inheritance just for yourself and loved ones to enjoy. The proportion will naturally depend on your circumstances but, in principle, it’s a great idea as it allows you to balance sensible saving and investments with some short-term enjoyment of your wealth.

Talk to us, we can help.